On this topic, I am seeing so many mistakes in financial economics across social media, but I will not go through them all. It suffices to note that very smart people have their minds turn to mush when this topic comes up, especially the “sell short” side of the matter.

There is also the “beware isolated demands for rigor” response. I should not have to demand anything. If you are pretty worried about AI, you should be dying (yes pun intended) to provide that rigor, whether or not it is provided elsewhere.

How about a new policy?: “All AI safety expressions of despair, grief, panic, anger, or insinuations thereof, with or without gifs, shall be accompanied by an estimated percentage of gdp footnote.” Would inject some real sanity into the discussion and drain out some of the all too rampant emotions.

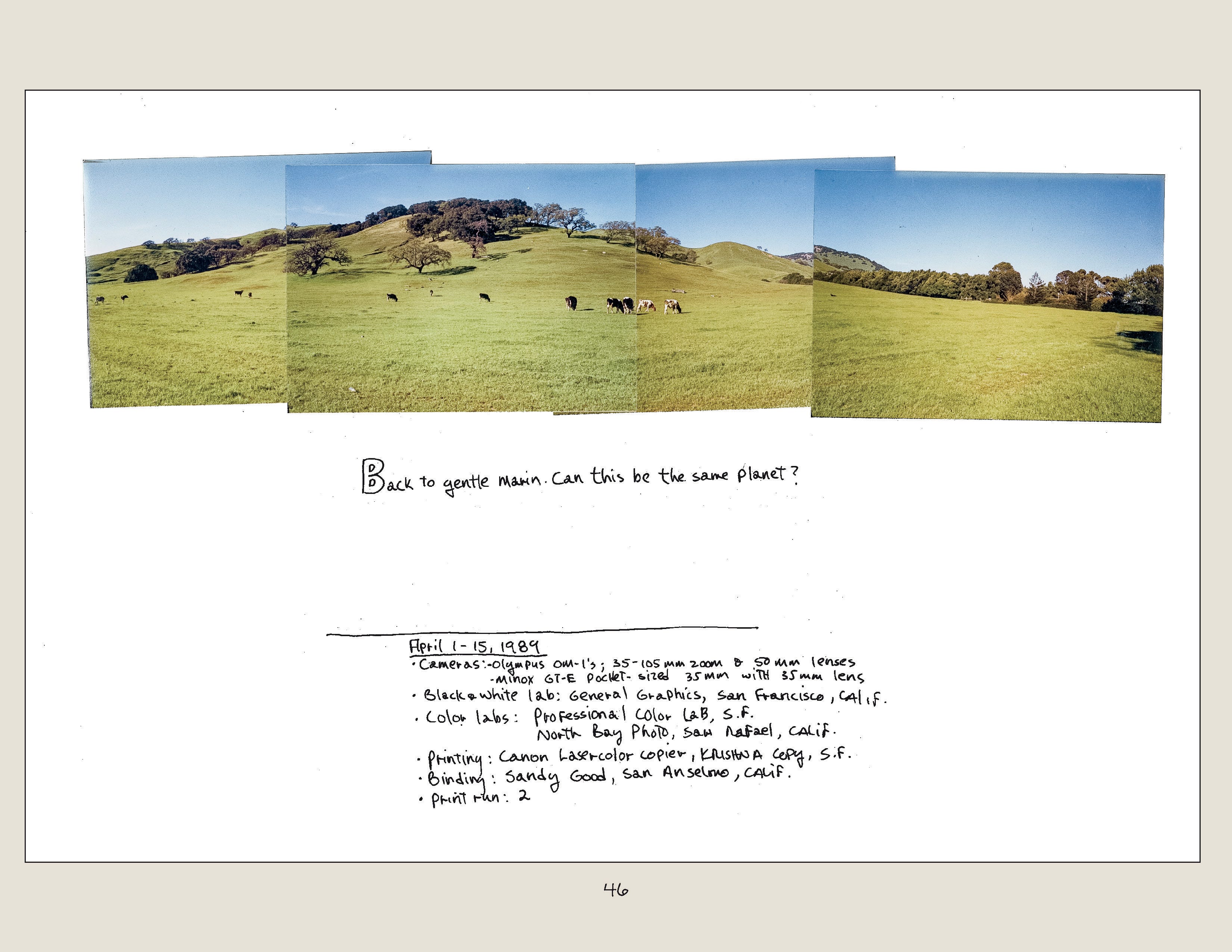

Note: When you get notice of this post via email,you have to click on the headline above to view these posts in a browser. This will give you the posts full-size. They are not legible at the small size in an email.

Or, just click on any photo, and the entire post will open in your browser.

I’m loving the (Tri-x) black and white film in revisiting this book. I understand why a bunch of my friends have gone back to shooting film. These ain’t no iPhone shots…

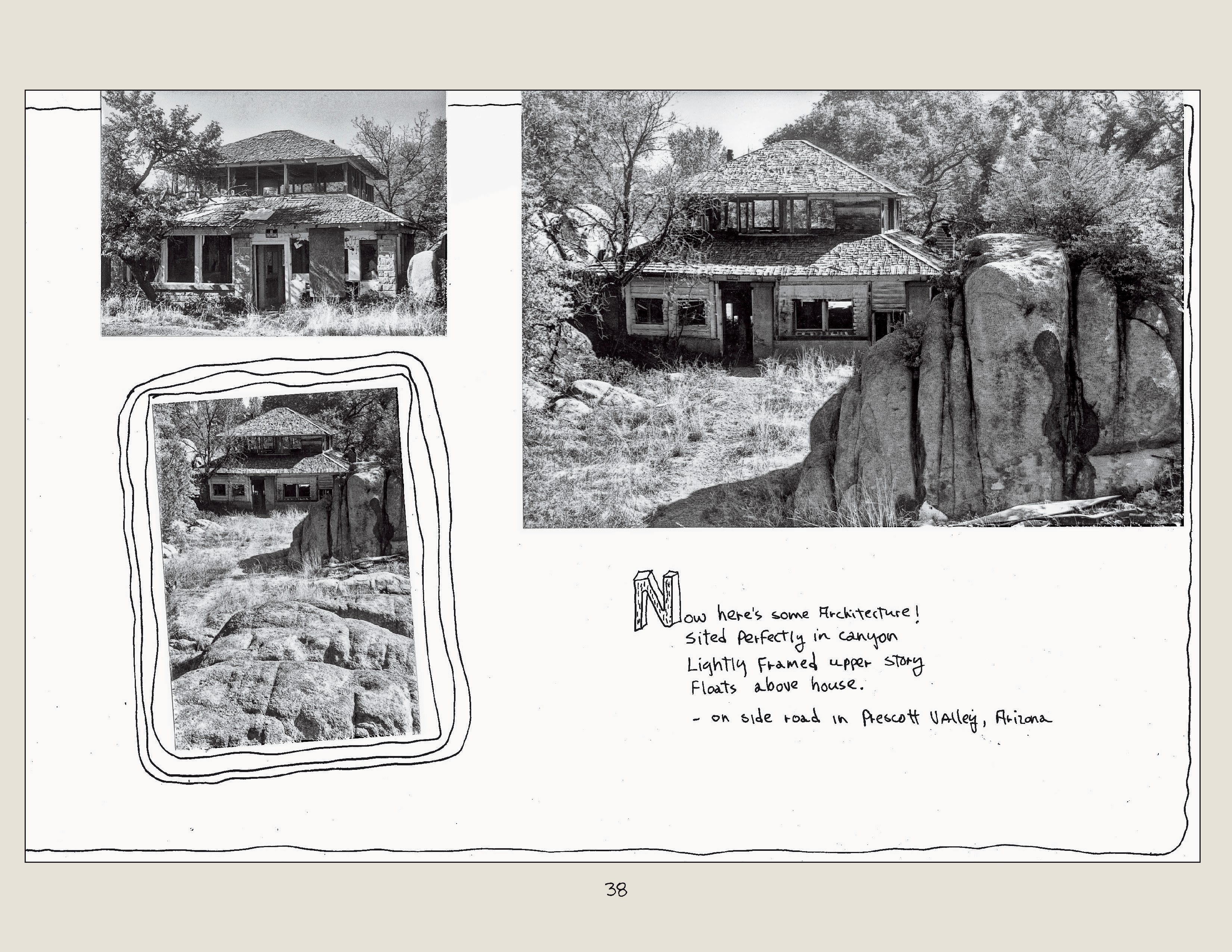

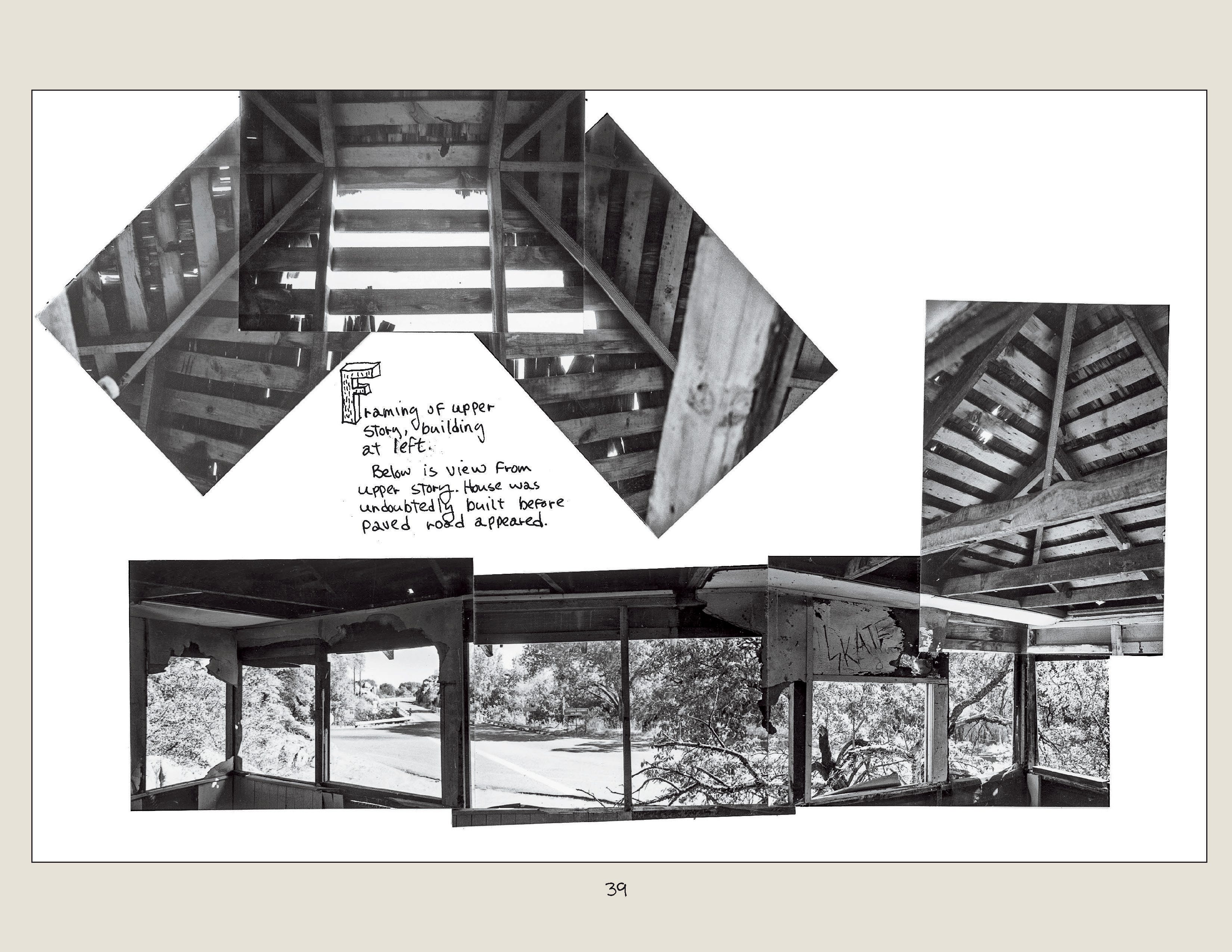

Architects and builders: look at how this building is constructed. It’s a beauty!

The gracefulness and symmetry of the two hip roofs, the placement of the building in the landscape (with the boulder), and the delight of the light-filled upper story with a 360 view. Architecture.

Live From California with Lloyd Kahn is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

I loved just about every part of America back then — as I went south, east, north, west. Good people all over in the ‘60s-’70s. I had the best vibes everywhere, and that in spite of the fact that I was a bit, um, hippie-ish looking. Good good good vibrations…

I’m looking at these shots, and interestingly, they look alive in spite of the fact they’re 4th generation:

Prints from Tri-X film

Pages of book copied on Canon Lasercolor Copier

PDFs made of pages

Pages loaded into Substack

Even on this electronic screen, I see an element of soul in the photos that’s missing in digital shots.

Guess what — intrepid reader who’s still with me — I’m gonna get back to doing the occasional one-off book; print run of one. (Actually, no print run.)

Plus I’m starting, for to do fliers, pamphlets to hand out for the first time since the ‘70s.

It’s so refreshing to put stuff together sans computer.

Finding cracks in the fabric of communication…

Thanks for reading Live From California with Lloyd Kahn! This post is public so feel free to share it.

Now that Abdul El-Sayed is the Democratic nominee for Michigan’s open Senate seat, the outcome of this crucial race will depend mainly on two things: Whether Republicans succeed in demonizing El-Sayed because he’s brown and a Muslim, and whether they succeed in demonizing him as a left-wing radical.

I will defer for the now the question of whether bigotry will be effective this year, although I will address it another day. What I want to address instead is El-Sayed’s signature issue — healthcare. Yes, El-Sayed advocates Medicare for All, a position the usual suspects denounce as “socialism.” I will get to the politics of his stance soon. Today, however, I want to talk about the substance.

We should be clear that El-Sayed doesn’t even call himself a socialist. On the contrary, he explicitly disavows the label, saying “I’m a capitalist who just knows about capitalism”. In fact, as I explained in a previous post, the policies that El-Sayed advocates qualify him as a social democrat, not a socialist.

Still, El-Sayed advocatesa system under which the government would pay almost all medical expenses. Isn’t that socialism?

Well, if that is the criterion then much of U.S. healthcare is already socialist. In fact, the government’s role is so large that U.S. healthcare is better described as partially privatized socialism than as anything resembling a free market.

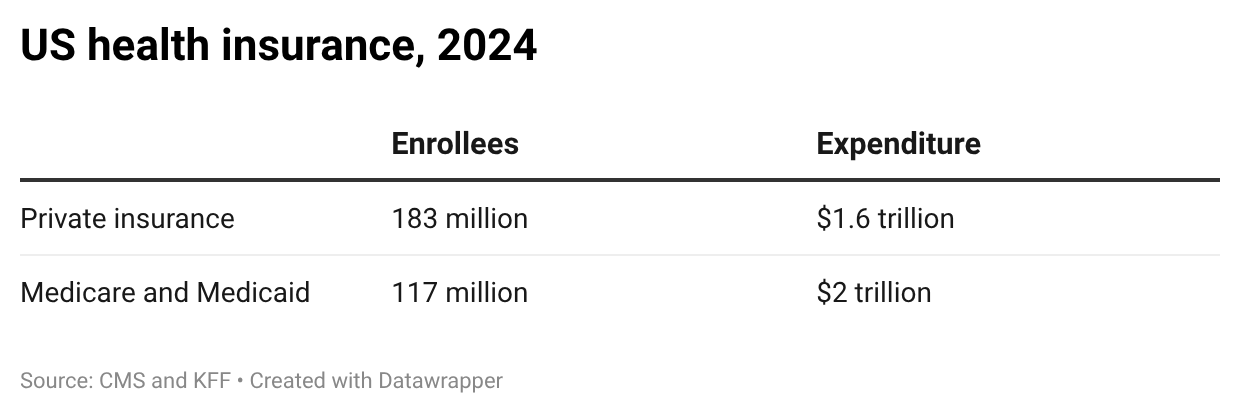

Let’s start with the raw numbers on health insurance, which pays the bulk of Americans’ medical expenses. Americans receive health insurance either from private companies or from public programs, overwhelmingly Medicare and Medicaid. Here’s what the breakdown of coverage and spending between private and public looked like in 2024:

While a majority of Americans with health insurance get it from private companies, well over 100 million of us are covered by government programs instead. And these government programs pay moretotal dollars for medical bills than the private insurers do.

Why do government programs that cover a minority of the population account for a majority of health insurers’ outlays? Mainly because Medicare covers seniors, and we’re expensive. Also, while Medicaid covers many younger Americans, disabled and elderly beneficiaries account for most of its spending.

Even by the raw numbers, then, U.S. health insurance looks as much public as private. But that understates the government’s role: Private health insurance in the U.S. is both highly regulated and heavily subsidized.

This is obviously true for the insurance coverage purchased by tens of millions of Americans through the exchanges established by the Affordable Care Act. But employment-based health insurance, which covers 161 million Americans, is far more of a government creation than most people realize. For employment-based insurance exists largely because of huge implicit government subsidies that come with major strings attached.

Here’s how that works. If your employer pays you $10,000, that’s taxable income. But if your employer pays $10,000 toward a company health insurance plan that meets certain criteria, it isn’t taxable. That’s a huge effective subsidy, running at more than $300 billion a year. Take that subsidy into account, along with the more than $100 billion per year spent subsidizing policies purchased under the ACA, as well as the outlays on Medicare and Medicaid, and net effect is that the government pays for more than two-thirds of Americans’ health insurance.

Granted, there are strings attached. Roughly speaking, employment-based health plans can’t discriminate based on medical history — that is, they can’t deny coverage to employees with pre-existing conditions — and they also can’t offer the plans only to highly compensated employees — a health plan that is only for the C-suite is considered taxable income.

So given the restrictions of the federal tax code, employer-based health insurance is a lot like Obamacare, which also prohibits discrimination based on medical history and provides subsidies to make insurance affordable to lower-paid workers. The fact is that virtually all of private healthcare insurance is already well under some form of government control through regulation and tax subsidies.

How should we think about this system? First of all, is Medicare socialist? Don’t tell anyone, but the way Medicare operates — it covers every senior’s medical expenses, whatever they turn out to be, while being funded by taxes that depend on one’s income — could be summarized by the old Marxist slogan “From each according to his ability, to each according to his need.” And back in 1961, when Ronald Reagan was the face of a last-ditch effort by the American Medical Association to block the creation of Medicare, he denounced Medicare as “socialized medicine” and warned that it would destroy our freedom.

In reality, American freedom survived until Jan. 20, 2025, while Medicare is immensely popular, with an 82 percent favorable rating in the most recent KFF survey. Medicaid, government health insurance for lower-income Americans, comes in at 73 percent. This is in sharp contrast to public views about private insurers, who are widely disliked if not hated and accused of denying essential care.

Furthermore, if Medicare is socialism, then the whole U.S. health insurance system, with the government paying most of the bills and placing conditions on private insurers, is almost equally socialist. If you insist on calling any program the government pays for and regulates socialist, then U.S. healthcare would best be described as a partially privatized form of socialism.

And one must ask, what is the point of the part that is privatized? Do private insurers add anything positive? Or are they simply parasites, skimming off money that could have been paying for care?

The case for viewing insurers as parasites is strong. Many Medicare benefits are now delivered via Medicare Advantage, that is, plans paid for by the government but run through insurance companies. MedPAC, an independent advisory commission, estimates that last year Medicare Advantage plans were overpaid by $84 billion, thanks to practices such as “upcoding,” in which patients’ health problems are overstated to get larger sums from Medicare.

Assessing the waste from employer-based insurance is harder, but most evidence suggests that private insurers have substantially higher administrative costs than Medicare does. Furthermore, the complexity of private insurance, with multiple payers all trying to deny care when they can, is a huge burden both on providers — doctors, nurses, and hospitals — and on patients.

What do private insurers offer to compensate for these costs? One must go through intellectual contortions to avoid the conclusion that they are, in fact, parasites.

Which brings me back to El-Sayed. In supporting Medicare for All, he’s basically calling for an end to the partial, parasitic privatization of a healthcare system that is already hugely dependent on public funding. When one looks at it that way, it’s not at all a radical proposal.

Admittedly, the political lift requires overcoming the opposition to higher taxes to pay for Medicare for All. Political realism rather than economics was the reason I and many other progressives supported Obamacare, with all its complexities, rather than demanding an immediate move to Medicare for All.

But the political calculus may very well have shifted since the 2000s, as Americans are fed up with a system of unaffordable premiums, rampant claim denials, and byzantine claim administration. Moreover, funding healthcare insurance through taxation would allow for a much more progressive distribution of the cost. That is, compared to the present system, middle-income households would pay less as high-income households would pay more. And the U.S. would stop wasting large sums on pointless administrative costs.

So let’s be clear: El-Sayed’s healthcare platform is perfectly reasonable on the merits of cost, fairness and health efficacy. And with private insurers never more hated, while millions of Americans are losing their health insurance, 2026 may be its time.

Meta are back in the open weights game! Muse Glimmer is a brand new 30B model under a clean Apache 2.0 license (a step up from the janky Llama licenses of old).

They claim to have optimized it for exactly the kind of things I'm looking for in a local model:

End-to-end Agentic Task Completion. Muse Glimmer achieves strong success rates on full-task benchmarks including DeepSearch QA, MCP-Atlas, 𝛕-Bench and SWE-Bench, which measure its ability to work within scaffolds, write and debug code, and resolve multi-turn requests from start to finish.

Reliable Tool Use. The model handles a wide range of function calls, invoking tools with precise schemas throughout extended workflows.

Multi-Step Reasoning. Muse Glimmer chains reasoning over long horizons, sustaining coherent plans across complex, extended workflows. [...]

I also tried it out with my llm-coding-agent plugin, running against a fresh checkout of Datasette with the prompt:

how does auth work?

Here's the response, at the end of a long transcript showing all of the tool calls it made to explore the codebase. I ran this using llm-lmstudio with this patch applied to upgrade it for compatibility with LLM 0.32.

I really like this size of model, because if a machine has 32 GB of RAM or more (mine has 128GB) it leaves plenty of space for running other applications at the same time.

Glimmer is a vision model, so I asked it to describe this image:

llm -m lmstudio/meta/muse-glimmer -a https://static.inaturalist.org/photos/714731804/large.jpg 'describe image'

The photograph shows a rocky, breakwater-style shoreline on an overcast day with a smooth, gray body of water and a faint dock/pier line in the soft-focused background.

In the foreground two large brown pelicans, Pelecanus occidentalis, are perched on the jumbled gray-white stones. They have the species’ characteristic long, down-curved yellow-orange bills with a large throat pouch, long slender necks and mottled brown-gray plumage on the back and wings. The pelican on the left is turned slightly toward the camera and appears to be preening or resting its bill against its chest; a pale, whitish patch is visible on the crown and nape and a small crest of feathers is raised. The pelican on the right faces mostly forward/right, its head up, bill pointing down and to the right, with the same pale head markings and the barred, darker wing feathers clearly visible.

Scattered among the rocks around the two pelicans are several much smaller dark birds — gulls/tern-like birds in muted brown-gray plumage. One dark bird sits on the far left on a rock, another brownish bird stands to the right of the right-hand pelican, a grayish bird with a reddish bill is in the lower right foreground, and a further small dark bird is at the extreme right edge of the frame.

The overall light is flat and diffused, giving the water and sky a muted, almost monochromatic palette that contrasts with the textured rock and the detailed feathering of the pelicans. The composition places the two big birds as the dominant subjects, framed against the calm water and the low, rocky perch.

Here’s a seemingly simple question: given a chunk of multi-line text, how do you split it and return an array whose members are the constituent lines of the text?

Hopefully, your first instinct is to reach for some sort of standard-library function, maybe something like the splitlines() method of Python’s str type. Because it turns out this “simple” question is actually pretty complex to answer! For example, quite some time ago I read a post by William Woodruff pointing out the surprising discovery that Python treats up to eleven different Unicode code points or code point sequences as indicating a line break.

At the time I meant to write about that, but a lot of other things started fighting for my time, and it’s only now that I’m finally digging it out of my drafts. Still, better late than never, so today let’s dig into some of the many ways there are to break a line of text and how they’ve been standardized and specified and ultimately wound up in the set Python uses.

In the beginning…

Once upon a time, there was ASCII. Of course there were other things before ASCII, and alongside ASCII, but for today’s discussion we really only need to go back to ASCII; if you want the full history of physical teletypes, how they evolved from typewriters and influenced character sets for computing and so on, I suggest Wikipedia. Here, I’m just going to gloss over and simplify a lot of that to focus on the topic at hand.

So. Once upon a time, there was ASCII. And it wound up being incredibly influential and important in computing, to an extent other early character sets couldn’t match. And because it was used on computers which used teletypes (basically electronic typewriters connected as input/output devices) as a user interface, it contained control characters for sending commands to the teletype. Such as a LINE FEED (byte value 0x0A) to advance the paper vertically to the next line, and a CARRIAGE RETURN (byte value 0x0D) to re-align the print head/carriage with the horizontal start point of the line.

These are often abbreviated LF and CR (or by their C-family escape sequences \n and \r, respectively), and you might think that since physically advancing a typewriter-style device to be ready to print the next line requires both operations, that would have just become the universal way everybody did new lines. Or at least the universal way everybody did them in English, or in the US, where ASCII dominated. Right?

Well, nothing is ever that simple. Physical teletypes apparently benefited from the two-character approach (as opposed to a single “new line” character) because it gave them time to physically move everything into the right position. But as virtual teletypes—“printing” to a television-like display instead of to paper—became more common, that was less of an issue. So there were multiple possible options for representing line breaks, and several of them showed up in historical systems. For example:

CP/M used CR LF. And so MS-DOS, which aimed for compatibility with it, used CR LF too. And so Microsoft Windows, which wanted to be compatible with MS-DOS, also used it.

Meanwhile, Multics chose to use just LF with no CR, and Unix went along with that choice.

But Commodore and Apple and many others went yet another way and used plain CR , with no LF.

This meant “plain text” was not easily portable between these various systems, since none of them could agree on how to represent a line break. Which led to one of my all-time favorite programming jokes, in the infamous “NOT the comp.text.sgmlFAQ” document:

Q. What’s an RE?

A. RE is an acronym for Record End, which is sort of like a newline, only different. Goldfarb’s First Law of Text Processing states that:

“… if a text processing system has bugs, at least one of them will have to do with the handling of input line endings.”

[The Handbook, footnote p. 321]

The Record End concept was introduced to make sure that SGML parsers don’t violate Goldfarb’s First Law.

Anyway, over twenty years ago Python tried (in Python 2.3) to smooth this over by introducing “universal newline” mode for opening files, which accepts all three options: a plain \n (Unix), or a plain \r (classic Mac), or an \r\n sequence (DOS and Windows) will all be interpreted as line breaks.

But even in ASCII there there are other ways of breaking a line. For example, at byte value 0x0CASCII includes the FORM FEED control character (FF, or \f). Which is not one of the traditional characters used by major operating systems as a “newline”, but nonetheless does cause a new line to occur: it moves to the next page (if necessary, by ejecting the current sheet of paper from the printer and feeding in a new one). And there’s also 0x0B, VERTICAL TAB (VT or \v): just as a “regular” tab (\t) causes a horizontal adjustment, a vertical tab causes a vertical one. So it, too, causes output to advance to another line (probably skipping several in the process).

And the C1 control characters added 0x85, the NEXT LINE character (typically abbreviated NEL), useful for translating back and forth between ASCII and IBM’s EBCDIC character set (which had “New Line” as a single character).

Then Unicode happened

Today we live in a Unicode world, and Unicode tries its hardest to catalog and standardize and describe how to work with all the world’s writing systems. Chapter 5, Section 8 of the Unicode Standard, “Newline Guidelines”, lists seven code points to recognize as causing new lines. Five of them we’ve seen already:

U+000A LINE FEED, from ASCII

U+000B LINE TABULATION, from ASCII’s vertical tab

U+000C FORM FEED, from ASCII

U+000D CARRIAGE RETURN, from ASCII

U+0085 NEXT LINE, from the C1 control codes

The CR LF sequence is also recognized, on systems which use it.

But the other two code points are new and were created specifically for Unicode:

U+2028 LINE SEPARATOR (which Unicode likes to abbreviate as LS)

U+2029 PARAGRAPH SEPARATOR (similarly abbreviated as PS)

The Unicode Standard explains that the traditional newline characters had started to become ambiguous, because of the rise of tools such as word-processing programs which implicitly broke lines to wrap them for display and so began using explicit “newline” characters to mean a paragraph break rather than a line break. So Unicode added two new code points whose purposes are explicit. And the standard says that “[I]n Unicode text, the PS and LS characters should be used wherever the desired function is unambiguous.”

And expanding on Chapter 5 of the Standard, there’s Unicode Standard Annex #14, “Unicode Line Breaking Algorithm”. As the name implies, this document formally specifies the line-breaking algorithm for Unicode, including defining things like which characters offer an opportunity to break a line, whether the break is mandatory, and whether the break would come before or after the character in question. It does this in a typical Unicode way: by defining a set of named properties and specifying which characters have which properties.

Two ways about it

But there are still three “newline” characters supported by Python that we haven’t seen yet, and they come from a place that might be surprising: Unicode Standard Annex #9, the bidirectional algorithm. And it’s OK if you’re wondering what that has to do with newlines, because it’s not immediately obvious if you don’t already know about it.

Some written scripts, like the Latin script this blog post is written in, are written and read left-to-right: the start of a line of text is on the left-hand side, and the end is on the right-hand side. Other scripts, such as Arabic or Hebrew, do the opposite, and are right-to-left. And so Unicode, which again wants to cover all the world’s writing systems and let you use any or all of them, has to support both left-to-right and right-to-left horizontal text direction.

But more than that, it has to support switching direction within a single piece of text. You might have something that’s in, say, Arabic but quotes something in Spanish in the middle of a line; that would require a short section of left-to-right inside an otherwise right-to-left text. Or you might be writing something that uses boustrophedon, switching directions on each line. So Unicode includes direction-control characters like U+200E LEFT-TO-RIGHT MARK and U+200F RIGHT-TO-LEFT MARK to handle this. But it also needs to know the scope of a direction change, and that’s where the last “newline” characters come in: the Unicode bidirectional algorithm says that “[t]he effects of all of these formatting characters are limited to the current paragraph; thus, they are terminated by a paragraph separator”.

So Unicode characters have, among their properties, a “bidirectional class” which influences how they affect the bidirectional algorithm. And the characters which act as paragraph separators for purposes of ending the effects of an explicit directional marker all share a common value for this: bidirectional class B. The characters with that class include quite a few that we’ve already seen, along with three more characters:

U+001C INFORMATION SEPARATOR FOUR

U+001D INFORMATION SEPARATOR THREE

U+001E INFORMATION SEPARATOR TWO

But these are better known by their original ASCII names: FILE SEPARATOR, GROUP SEPARATOR, and RECORD SEPARATOR. ASCII provided these to help represent data structures in memory and on storage media. Today it’s not as common to try to use control characters for this purpose, though they do have the virtue of being rare in actual text, unlike other common delimiters such as tab or comma.

End of the line

And now, after looking at multiple character sets and five Unicode technical documents, we can finally state clearly what’s going on in Python.

Python’s splitlines() treats ten different code points, and one multi-code-point sequence, as causing a line break. These are:

The sequence U+000D U+000A (CR LF).

The four code points which have line-breaking property BK (Mandatory Break (Non-tailorable)): U+000B LINE TABULATION , U+000C FORM FEED, U+2028 LINE SEPARATOR, and U+2029 PARAGRAPH SEPARATOR.

The one code point which has line-breaking property CR (Carriage Return (Non-tailorable)): U+000D CARRIAGE RETURN.

The one code point which has line-breaking property LF (Line Feed (Non-tailorable)): U+000A LINE FEED.

The one code point which has line-breaking property NL (Next Line (Non-tailorable)): U+0085 NEXT LINE.

The three code points which don’t have any of the above line-breaking properties, but do have bidirectional property B: U+001C INFORMATION SEPARATOR FOUR, U+001D INFORMATION SEPARATOR THREE, and U+001E INFORMATION SEPARATOR TWO

Which is also exactly what’s stated by a comment in the CPython source code accompanying the list of individual code points that are considered to break lines, but hopefully now you have a better understanding of what that comment means and how this particular set was arrived at.

One thing that bothered me about Imprint’s product after joining was our lack of passkey support.

Passkey support is a rare opportunity to increase resiliency to phishing attacks

while simultaneously reducing login friction. If it’s good for our members, our partners, and our product,

it felt like something we should have already shipped.

Nonetheless, it was hard to get it onto the roadmap alongside everything else we were working on.

To dig into passkeys, I started sketching out the implementation as a side quest.

Some iterations later, I had something implemented behind a disabled feature flag for team review.

At that point, most problems had a concrete solution implemented, and the remaining issues

were messy intersections between passkey implementation and user experience.

Issues remained, but the tangible implementation made tradeoffs explicit, and we were able to work through them.

Soon thereafter, we launched passkeys to a small group in our web experience,

iterated on feedback, finalized the details, and brought those details forward to our native

mobile experiences as well.

It never got onto the roadmap, but it did ship.

Our passkey release planted a seed for me, but it required another experience to fully germinate.

We had a discussion about hitting a date for a product extension we’re developing.

Our conversation kept anchoring on the idea that pulling in a date was dependent on pushing out dates for other

projects. Presenting two conflicting projects as requiring timeline tradeoffs wouldn’t have caused me

to blink an eye five years ago, but in this conversation it inspired a sort of instinctual revolt:

with modern development techniques, I believe very few projects are essentially constrained by execution bandwidth.

Some are constrained by approvals, others are constrained by cross-team and cross-functional handoffs,

and many are constrained by missing decisions, but almost none should be constrained purely on time.

Shifting blocks of time across projects to speed up delivery felt wholly divorced from the reality

I work in.

Grappling with my frustration for some time didn’t lead to a profound awakening, but

it did help me bring together my thoughts about how effective modern organizations operate.

The modern organization operates most effectively by orienting itself around highly empowered teams who broaden their capabilities to

absorb cross-team and cross-functional handoffs,

can rely on automated harnesses to address most remaining cross-functional approvals,

and accelerate high-quality decision making through rapid prototyping.

The premise here is an old one, but AI-tooling has shifted what’s possible in remarkable ways.

Reducing handoffs with team and individual accountability

In 1975, Fred Brooks’s The Mythical Man-Month

warned us that adding individuals to a late project makes that project even later rather than speeding it up.

However well-understood this is, it remains extremely common for leaders to repeat this mistake, even today.

My personal theory is that most leaders performing the “ask for more staffing” gambit intuitively know they are optimizing to

“get stuck” in a way that shifts responsibility off them because they didn’t get the requested funding,

rather than that there is no way to accomplish the task at hand.

Even if teams avoid the simplest versions of the mythical man-month’s trap, organizations that operate through

strict ownership of defined boundaries introduce the same problem.

Well, of course your team can’t launch that without approval from the architecture team and the security team and performing

a user research study. That’s not really your team’s ownership area, you’ll need approval from the membership accounts team, at a minimum!

Agile, with the idea of collective code ownership, rejected this idea in principle, although certainly it remains messy in practice.

Even with strong AI-enhanced workflows, I still find human review of load-bearing technical decisions (e.g. a decision that will

meaningfully impact subsequent decisions) to be extremely valuable. This is why the highly-empowered team model is an effective

compromise: there needs to be an experienced engineer whose perspective is infused into the architecture, who shares the team’s

context, and who is aligned with the team’s priorities. This creates space for earlier career folks to be highly effective,

while also allowing teams to largely operate independently across complex, intersecting goals.

The final piece of driving accountability is rejecting the argument that a problem is too confusing or too hard for someone to know the consequences of their work.

There are a lot of hard problems, and that’s what makes creating software such an interesting job.

However, in a world with infinite feedback readily available, even if that feedback is of inconsistent quality,

getting surprised or being unable to unpack a problem is an algorithmic gap in how work is being approached.

Learning how to manage that gap is a core part of being an engineer, and something we are accountable for learning.

To be explicit, the argument isn’t that folks should be flawless: mistakes are fine, even laudable in some cases.

Laudable mistakes are almost always couched in a web of derisking, often feature flags, to make them inexpensive.

If someone isn’t increasingly effective at derisking their decisions throughout their career, then they’re not

being accountable for their impact as an engineer.

The above section has been fairly standard advice for decades, but I believe AI-tooling has substantially changed three dimensions of this approach:

Maintained context in e.g. AGENTS.md files can improve the overall approach of the company working

on a given area. It’s very hard to train an entire company, but today you can get many of the outcomes

of training by manipulating centralized context. This makes it far easier to operate decentralized teams

than in prior eras.

Inconsistent patterns in a codebase will “poison” an LLM’s context window with bad patterns,

but it’s never been easier to simply remove those bad patterns from the codebase.

Bad patterns within your codebase are largely a problem you can choose not to have at this point.

This further simplifies operating decentralized teams, especially if you love introducing tighter typing and linting.

Which I do.

One high context engineer can scale themselves across a team’s scope much more easily than before

by using LLM-tooling to investigate, debug, monitor and influence agent development.

The broader this engineer’s judgment extends, the more effective they’ll become.

I don’t think that any of design or product or engineering are going away,

but individuals whose judgment spans across multiple of these fields

are increasingly impactful on their teams because they can breeze through

the easy cross-domain problems rather than get hung up on them.

In aggregate, I believe that these changes in degree become a change in kind for running an empowered team.

Minimize cross-functional dependencies with relationships or escalations

Even if code ownership is shared, it can become impossible to move forward if there’s enough cross-functional

permission required to make changes. To a small extent this is due to inherent misalignment in incentives across

functions, but it’s much more driven by incompatible priorities.

Where possible, it’s ideal to embed functions into a common pod to align priorities, but in an era of lean teams,

that’s not a particularly accessible solution.

Instead your two most likely solutions are the same ones that have always been there.

First, building relationships across functions to help get your project unblocked by

a helping hand from within that function. Second, an effective executive team is able

to make collective tradeoffs–and share some of their treasury of cross-functional relationship merit–to

unblock a given project.

Now, however, I think we finally have a playbook for speeding up cross-functional approval

in a meaningful way, which is providing function-specific harnesses that can perform elements

of their function’s work, especially of the approval variety.

I don’t see substantial adoption of this technique yet, but I see it coming, and Imprint has spun

up an internal AI team to iterate our way through deploying this approach. Hopefully we’ll be writing

about our learning there in a month or two.

Our goal is that every function has a centrally managed harness that can perform an increasingly large portion

of their team’s work, prioritizing the sorts of things that require cross-team approvals.

They would have a collection of general tools–e.g. search indexes of their work corpus–and also very

function specific tools–e.g. access to a tool like Zip for financial approvals on the Finance team–along

with the ability to provide skills and direction to the harness.

Assuming this idea works, this harness will become a shim on top of functions to further allow teams to

focus on the highest value work rather than getting caught up in the least interesting approvals.

Eliminate decisions through the iterative application of judgment

With less accidental complexity slowing down our organizations from cross-team

and cross-functional dependencies, we still have one very large remaining:

deciding what software to write.

Software is not, as some argue today, free, but it’s no longer constrained on

implementation weeks but instead on correct decisions.

Grounding this in an example, for an upcoming release we found ourselves grappling with

implications of changing how applicants applied for a new credit card.

There were concerns that we didn’t have enough weeks to implement the change.

However, the actual work to be done was roughly two weeks, and we were talking about

the initiative taking two months. The gap between the two weeks and the two months

was a dozen ambiguous decisions. Those proposing the longer timeline assumed we’d

continue making decisions at the current decision-making pace, resulting in the longer schedule.

There was some discussion around how we might find that number of months to complete the project.

Treating decision-making speed as a fixed constant

oriented the discussion around a complex, low-value workstream of deciding the relative

priority of other tasks we were currently working on and then reranking them to free up more calendar time.

But we were never constrained on calendar time, what mattered was accelerating the pace of high-quality decision-making.

In my experience, calendar discussions are another way that folks deliberately get stuck, because no company ever has a central

list of the true priority of every task. Asking for that non-existent list shifts accountability for forward progress

off the asker, but it’s a fundamentally unreasonable thing to ask for. Thinking about things from

a CPU scheduling perspective: any scheduler that tried to centrally orchestrate priority within every thread

would be extraordinarily slow and stuck all the time; it’s only by locally determining priority–often

through extremely crude methods–that things move quickly overall.

Decision-making at a fixed degree of complexity hasn’t gotten easier with AI-tooling

but AI-tooling has dramatically reduced the complexity of most decisions I see in practice.

Going back to the passkey problem, trying to make those decisions from a blank slate was very

difficult. I was simply too ignorant of the handshake’s constraints to correctly decide the UX details.

However, I was able to iterate through the open decisions as a side project, until the answers became obvious.

The answers became obvious not because I got smarter–I didn’t get smarter–but because iterative

exploration discarded many of the initial options until the inherent constraints of passkeys and

our user experience simplified the problem.

Prototyping–e.g. the iterative application of judgment–can turn most complex problems into a series of simple problems,

and the rate of prototyping today makes it a substantially more accessible strategy than in the past.

Yes, prototyping has always been a well-received solution to validate ideas, but it used to be expensive

enough that many teams didn’t take advantage of it, but these days I think it is the most accessible way

to find high-quality decisions within an ambiguous problem space.

A roadmap of decisions, not on dates

Combining all of these ideas, the world we live in is increasingly constrained by

access to high-quality decisions. Rather than talk about scheduling software around software,

we should be fixated on the idea of accelerating making high-quality decisions.

Every hour we spend deciding priorities or timelines is a distraction from making the next decision.

As an ending caveat, this isn’t an argument that we shouldn’t have dates on projects.

Dates are the external interface for coordinating across companies, so you still need dates.

However, I think teams are better picking a plausible, slightly conservative external date

and then entirely ignoring that date internally. Instead, they shuold

focus on the list of decisions to be made, and work through

them directly. Dates, global priorities, stack ranked items… An engineer who doesn’t know the release date

can still ship.

If you haven’t heard, the Trump administration, on Monday, announced an executive order that, in reality, would decrease the uptake of childhood vaccines. Among other things, it calls for breaking up the MMR vaccine into three separate shots–even though there is no manufacture of single shot measles, mumps, or rubella vaccines–along with administering each vaccination at a different medical appointment. The unannounced goal is to make it harder for parents and kids to find the time for vaccination; it also would overwhelm doctors’ offices, and, to the extent there would be co-pays, will cost parents more. The order also calls for ending administration of influenza and COVID vaccines to children.

All of this is in service to the debunked hypothesis that childhood vaccines cause autism. At the same time, the U.S. is experiencing its largest outbreak of measles in decades.

Some people have been pointing out that this is an executive order, and therefore we should calm down. Trump has been stymied in the courts over similar attempts, states are adopting pre-Trump CDC guidelines and so on. So Trump and his minions won’t be able to do as much damage as they would like.

But The Discourse, thanks to the Fauci hearings, spent a couple of weeks arguing about how Fauci’s and others’ statements during the pandemic might have undermined confidence in public health. But compared to that, this executive order is a deliberate attempt to undermine one of the most successful public health interventions in history during the worst measles outbreak in years. To say the least, that too undermines confidence in public health.

We can hope–and if you’re not a resident of the mainland colony known as the District of Columbia, you can call your congressional representatives*–that this fails in terms of policy and politics.

*States are going to be really important in combating this, so call your state representatives too.

NME: Harry Potter fans have succeeded in moving a construction project that would have originally gone through the “grave” of the character Dobby.

The 125-mile Greenlink power connector, which costs £430million, is intended to link power between the UK’s National Grid and Ireland, running between County Wexford and Freshwater West in Pembrokeshire.

However, the latter site is known to Potter fans as the site of house elf Dobby’s grave in the film Harry Potter And The Deathly Hallows, and contains a pile of stones with the words “here lies Dobby” that many flock to…

All I can say is that Voldemort would never have put up with this shit.

Abstract: How is AI transforming decision-making in modern conflict? This study provides a unique empirical window into that question by deploying a high-fidelity replica of an AI decision-support system (DSS) used in military targeting. After reconstructing the interface and functionality of the real-world system, we tested its impact on combat decisions in two experiments involving 2,015 Israeli military personnel. Contrary to widespread fears of automation bias, we find strong evidence of algorithmic aversion, especially in scenarios involving high collateral damage. Yet we also show that integrating “explainable AI” features reduces algorithmic aversion and promotes more thoughtful evaluations of algorithmic recommendations. These findings challenge prevailing assumptions, revealing that trust in military AI is dynamic, varying with individual predispositions, perceived operational stakes, and the informational features of the interface. By grounding normative concerns in empirical evidence, our study offers critical insight into the integration of AI in warfare and underscores the enduring importance of human agency in high-stakes military decision-making.

Sam Bowles and Wendy Carlin propose that we should think of civil society as the third leg in regulating economic life, along with government and markets. (They use kidney exchange as an example to indicate what they mean.)

"Abstract: Interactions in civil society – in firms, families, neighborhoods, identity groups, and other face-to-face settings – have in common that relationships are personal and enduring, and as a result, identity and other-regarding preferences are important motivations (for better or worse). Here we add civil society to markets and states as a third form of governance of the economy, creating the governance triangle. We provide evidence that themes related to civil society have assumed substantially greater importance in economic research since the 1970s. We use a standard principal-agent model of employment in private firms to reveal three characteristics of interactions in civil society: the role of face-to-face interactions, social norms, and the private exercise of power. We show that market failures and other coordination problems can sometimes be more successfully addressed by civil society than by state or market governance. Civil society may have comparative institutional advantage where information available to state and market actors is limited, restricting the reach of complete contracts and enforceable government regulations, conditional on conflicts of interest being modest. When based on us-versus-them forms of identity, however, civil society governance may promote preferences antithetical to a liberal and democratic society."

"To illustrate the meaning of points in the triangle, we have placed the kidney exchange model proposed by Alvin Roth and his collaborators (the red dot) in the governance triangle ((Roth et al 2006).) They designed a mechanism connecting those needing a kidney replacement to altruistic donors of kidneys. Such donors are most often an immediate family member of someone whose kidney is not a match for their loved-one needing the transplant. Roth’s algorithm enables long chains of unrelated matched donors and recipients, thereby widening access to transplants because they do not have to be conducted bilaterally (the donor giving to a particular match) and contemporaneously.

"As an illustration of the nexus of synergistic institutions in the triangle, we represent the kidney donor mechanism, the red point, by a weight of 0.3 on the state (which regulates the exchanges, including prohibiting sales), 0.2 on the market (which provides associated medical services), and 0.5 on civil society (for the centrality of altruistic and ethical motivations underlying the initial contribution of the kidney.)... By relating the characteristics of behaviour and the allocation mechanisms involved to the three pure types, other institutions and policies can be located inside the triangle."

########

Note that this representation in a triangle is in a barycentric coordinate system, which has only become a readily recognizable tool in various applications in economics in the last half century or so. Wikipedia dates their introduction to 1827.

One of China's most used rockets, the Long March 7A, exploded a little more than a minute after lifting off on Monday evening, local time.

The medium-lift rocket's payload was classified, but it was believed to be a military communications satellite. The rocket's liftoff from Wenchang Space Launch Site appeared to be nominal, but publicly captured videos (such as this one) showed that the rocket's first stage exploded about 1 minute and 20 seconds into flight.

The Long March 7A rocket was developed by the China Aerospace Science and Technology Corporation and is operated by the state's space agency. As of Monday night in China, state officials have not commented on the explosion.

Below you will find my latest roundup of great new music. As always, I cover a lot of ground, drawing on a range of genres, generations, and geographies.

Happy listening!

Please support my work by taking out a premium subscription—for just $6 per month (even less if you sign up for a year).

Horse Lords: Demand to Be Taken to Heaven Alive! Cool Microtonal Jams

Back when Horse Lords made my best-of-year list in 2020, I struggled to describe this Baltimore ensemble’s genre—and eventually came up with a clumsy circumlocution: “If La Monte Young Ran a Funky Microtonal Rock Jam Band.”

Six years later, I still can’t give a better description. But, against all odds, this kind of quirky music is now going mainstream—witness the quick rise to crossover acclaim of Angine de Poitrine (discussed here), a band that’s relying on a similar aural toolkit.

I never dreamed that microtonal odd-metered tunes would come so far. But this group’s latest release will show up on many best-of-year lists in 2026 (mine included). Here’s a deep draught for the adventurous.

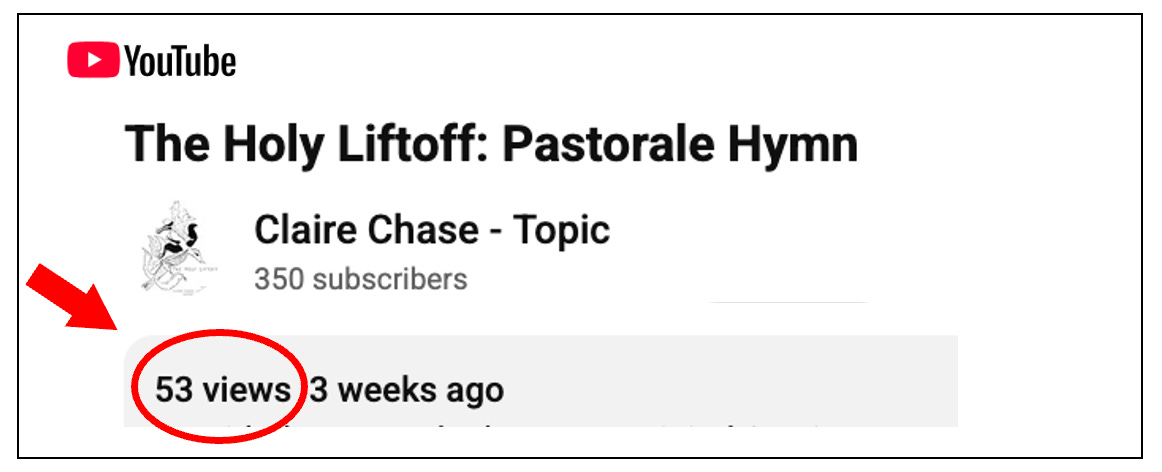

Terry Riley / Claire Chaise / JACK Quartet / Samuel Clay Birmaher: The Holy Liftoff Chamber Music for Eight Flutes, String Quartet, Stones, and Wind

Terry Riley, now age 91, is still such a vibrant force on the music scene. Over the decades, he has done it all—breakthrough classical compositions, jazzy piano, ecstatic chanting, psychedelic trance-rock, alternative tuning systems, and much more. (In the future, I’ll share a list of my favorites from the course of his variegated career.)

Riley started work on The Holy Liftoff in 2022 at the invitation of flutist Claire Chase (also a Harvard professor and MacArthur ‘genius award’ winner). It began, according to her website, as “an open-score sketchbook of brilliantly colored drawings for multiple flutes.” Samuel Clay Birmaher helped turn it into a “multidimensional work blending through-composed material, graphic notation, evocative artwork, and Riley’s signature open-form scoring.”

If those descriptions sound confusing, just bypass the verbiage and go straight to the music. It sounds like a celestial flute choir inviting you into a dream landscape.

I’ll share another track, but first look at this travesty.

This music is reaching a smaller audience than karaoke night at your local pub. That is why you need an honest broker—because the media and music world won’t tell you where greatness truly resides.

Okay, here’s one more track from The Holy Liftoff. Forget SpaceX—this is my type of launch into the empyrean.

Claude and I planted 100 known errors into 10 open-access psychology papers and then ran them through frontier models and two commercial AI review tools. In brief:

The best single system caught 71 of 100 errors, while the worst caught 30.

Pooling every system’s output caught 93 of 100. Models are only partly correlated in the errors they find, making ensembling a big lever for finding issues in papers. Check your papers against multiple models!

Seven errors could not be caught by any system. All were omissions — information deleted from a paper rather than mistakes inserted into it.

Refine.ink contributes more unique catches than any other single system, though it’s expensive.

I didn’t measure false positives and I don’t know how this error distribution compares to the distribution of errors in real papers.

I’ve made the papers, errors, model outputs, and the full experiment log public. I hope people can build on this work to create a comprehensive eval benchmark across disciplines.

That is from Paul Litvak, here is more. Note that is not even using the very latest generation of models.

We trace the family origins of Members of Congress (MC) born between 1830 and 1950, linking each MC, their parents, and their brothers to the complete-count censuses. Future MCs have always been economic outliers. By 1940, close to 60 percent of MCs aged 18–40 held a college degree, against under 5 percent of comparable young men outside Congress. In the 19th-century censuses, MCs as adults held roughly three times the wealth of demographically matched controls. They also come from economically elite families: their fathers earn more, attain more education, and hold more wealth. The brothers of future MCs sit between the population and the MCs themselves. Across the socioeconomic measures we compare, we calculate that roughly half of an MC’s adult premium is shared with his brother and the other half is his own. Even as the American economy and political system have changed, the family background gap has widened over the last century and a half. Wealth, household servants, and four separate occupation-based scores all show the gap holding or growing across cohorts. We study four Progressive-Era reforms in a triple-difference design—women’s suffrage, the secret ballot, direct primaries, and the direct election of senators—and none produce detectable shifts in who reaches Congress. Our results document a Congress drawn from the most fortunate families in American society in every cohort we observe.

For the first time, baseball fans can take in all the action of

“Friday Night Baseball” live in Apple Immersive on Apple Vision

Pro, leveraging 3D video recorded in 8K with a 180-degree field of

view. On August 28, viewers with Vision Pro will experience the

iconic Red Sox vs. Yankees rivalry from unique camera angles that

place viewers right in the game, immersed in the drama of each

at-bat, the celebrations in the dugout after a big hit, close

plays at the outfield wall, and more.

The experience features bespoke commentary from Paul Severino

(play-by-play), Xavier Scruggs (analyst), and Michelle Margaux

(sideline reporter); dedicated replays; and an immersive graphics

package that includes team lineups and stats floating in the

viewer’s space. During breaks in the action, the broadcast remains

live, immersing viewers in the stadium experience from all angles

as ambisonic microphones capture sounds in Spatial Audio.

Hot damn, they even picked the best rivalry in sports to kick it off.

I’m really unhappy about this, both for my role in spreading a

false story and because I think it will hurt the cause of

reforming App Review. I know there are many crazy rejections and

have experienced some first-hand. This story was believable

because of that well-known history and because Godier didn’t seem

like a nobody trying to get attention — he was the developer of

another highly regarded app. But now people are going to point to

true developer stories and accuse them of being fakes, too.

I’m seeing email after email suggesting these users built a thing

they’re truly passionate about. But if we can’t trust that this

passion is real, legit, and from the heart, we’re in trouble.

Take a step back. Is this thing you built a reflection of you?

I think it’s fun and exciting that I’m getting a lot more emails about a lot more new apps. But a fair chunk of those emails are themselves clearly written by an AI chatbot. It’s so obvious. Those go straight in the trash.

Kalley Huang, reporting from San Francisco, and Ana Swanson, from Washington, for The New York Times (gift link):

Apple, which has cited the memory chip shortage for recent price

increases, is working with other consumer electronics companies to

push for permission to buy memory chips from China, which faces

certain restrictions, seven people said.

Apple was in talks in 2022 to buy memory chips from Yangtze Memory

Technologies Corporation, or YMTC, but those efforts fizzled under

pressure from U.S. lawmakers.

Many officials appear unsympathetic to Apple’s desire to buy

Chinese chips, because the company has promised for years to move

more of its supply chain to the United States but has made only

small steps toward that goal, four people said. Other critics of

the plan said that China was also experiencing a similar chip

crunch, and had proved itself to be a risky supplier when it

restricted its mineral exports last year.

Apple has been testing memory chips from China’s CXMT across

product lines including iPhones and MacBooks, according to people

familiar with the matter, as the U.S. company addresses a memory

crunch during the artificial-intelligence boom.

Apple has held early talks with CXMT about supplying components

with the goal of using them in some devices sold in China, the

people said. Apple hopes to win the White House’s blessing to do

business with the Chinese company. [...]

Apple often tailors components to its devices to maximize

performance. Using standard CXMT memory chips could force Apple to

redesign certain parts of its products. Industry analysts also say

CXMT’s technology still trails its foreign competitors, in part

because the company’s access to the most sophisticated chip-making

equipment is restricted.

At present, CXMT wouldn’t be a panacea for Apple. The Chinese

company has maxed out its production capacity this year, leaving

little room for new international clients, the people familiar

with the matter said.

The gist of both reports is that just like in 2022, Apple might not get permission from the U.S. government to use Chinese RAM, even for devices sold in China. And, even if they do secure permission, it might not actually help much with the supply crunch.

Sometimes I write a post which is about information that is not new or secret but new to me. This is one of those posts. I’m sharing it because the information is new to me and I suspect many TPM readers. It’s helpful for me in thinking about the rise of the Democratic Socialists of America as the most visible left faction within the current Democratic Party. Recently I noticed that many or most of the DSA elected officials who’ve achieved some level of electoral success have been denounced, censured or rejected by the local affiliates or council who endorsed them in the first place. Along similar lines, the national DSA is consistently more doctrinaire and left-wing not only than it’s candidates but its local chapters in the major metros where its power is strongest. This isn’t surprising or really new. It’s a general pattern for ideologically-based organizations, an unsurprising feature of the tensions between ideology and complex electorates.

Back to those prominent DSA-backed politicians. I and many others have argued for a while that “socialist” seems more a matter of branding for a lot of DSA candidates, whereas the actual policies and positions sound a lot like pretty ordinary New Deal-style liberal-labor politics. Of course, what counts as “socialism” is wildly over-determined. You’ve certainly see those memes that show like the Socialist Party platform from the 1910s or 1920s and it mostly matches things we take for granted or did take for granted as the mid- and late-20th century New Deal state.

I note all this because we are all or all should be looking for ways to stitch together Democratic Party unity for critical elections in 2026, 2028 and beyond. If some differences are more matters of degree than kind, unity in diversity becomes more possible.

It’s with this in mind that I started looking more closely at Megan Romer, the national co-chair of the DSA. There are two co-chairs but, for whatever reason, Romer is the one who seems most visible. Romer is part of and a leader of some sort of something called the Red Star caucus of the DSA. As the name suggests, this is considerably more left-wing than anything we might call left/New Deal. The caucus defines itself as …

… a Marxist-Leninist caucus in DSA. Our primary goal, the goal which informs all of our organizing work, is to abolish capitalism and, ultimately, to achieve communism. We do not believe that capitalism can be reformed into socialism – it must be overthrown and replaced.

They go on to say that they see the DSA not as a conventional party and certain not as a faction within the Democratic Party but rather a vehicle or incubator for creating a vanguard revolutionary party.

We do not specify exactly how this party will emerge, but we believe DSA can foster its creation — DSA’s resources, broad membership, organizing ethic, and robust democratic processes make it, out of all existing US socialist organizations, the best incubator for such a party.

I quote this from Points of Unity, Red Star’s statement of principles on its website. There’s a lot more but it’s all pretty standard from a Marxist-Leninist viewpoint and outlook. As you’d probably expect, a major theme of Red Star’s politicking is attacking AOC as a capitalist running dog who has exploited DSA for careerist ambitions.

In any case, I’m not shocked by any of this stuff. I was born in and grew up around a lot of political radicalism. That probably shapes a lot of my political outlook. This stuff is as old as the hills. And I generally don’t have a lot of patience for making a big deal about tiny radical sectarian groups trying the standard burrowing-in tactics on larger left-wing parties. But this seems a little different. As I told someone yesterday, you can’t really say this is some malign cherry-picking among the countless caucuses operating under the DSA banner or a Fox News-worthy attempt to elevate random weirdos or extremists to discredit Democrats or the political left generally. Romer is the head of the national DSA. (Technically, she’s the national co-chair. But we seldom hear about her co-chair, Ashik Siddique.)

One of the ironies of this is that as terms developed over the first half of the 20th century, “socialism” (in the sense of socialist parties and so forth) generally became self-identified as socialist over and against the anti-democratic elements of communism which, of course, also claimed the socialist label. Old news for people who know this history but a lot of the most intense anti-communists were socialists, though that can seem odd to those outside these sectarian debates. Indeed, the DSA, which Michael Harrington helped found in 1982, was at the forefront of that element of socialist politics. There’s a reason “democratic” is there at the front of the label.

This is definitely suboptimal for Democrats or the anti-Trump opposition. But this is about more than optics. Strong civic democracy is what I think a lot of us are trying to rebuild in this country. We don’t support it as some off-the-shelf antidote to Trumpism but because that’s what we believe in, and only a rebirth of a vital civic democracy can bring us back from this moment. This vanguard, Marxist-Leninist revolutionary party claptrap is the polar opposite of that. It’s the seed corn of left-wing authoritarianism. For me personally, it’s difficult to separate a lot of this from what amounts to revolutionary cosplay. No, I don’t expect workers’ soviets to be taking power in any of our cities. More to the point, this isn’t meant to delegitimize or attack the various candidates running under the broad DSA banner. As I noted above, some of this is par for the course. A certain kind of person focuses on actual politics and getting elected. Others focus on grabbing slots on committees and arguing over manifestos. But Marxist-Leninist vanguard parties are not some version of New Dealism. We should be aware this exists as a real force in the national DSA. And that is a problem.

One of our great doctrines here in the Editors’ Blog is that all power is unitary. Lose or gain it in one place, and you lose or gain it in equal measure everywhere else. That’s catching up with Donald Trump. He got into the Iran War as a way to escape the emotionally crushing experience of declining popularity and power at home. But his ebbing power went with him to the Persian Gulf. And now it’s arrived in Israel, too. This was obscured for a while by the fact that the U.S. has almost unimaginable military power and a constitution which, as it has evolved if not how it was originally intended, puts almost no short-term limits on a president’s ability to wage war. But the two were always umbilically connected. It was the pain of bad news at home that spurred Trump to jump so recklessly into his Iran debacle. And it is the same unpopularity that has him so desperate to end high gas prices and inflation before the midterms. They’re all connected.

Trump has no poker face. To live in Trump’s era is not only to see his inner life but to be engulfed by it. It’s hard to think of a case in which the deciding player between warring powers has more clearly signaled his desperate desire to get out of a conflict on almost any terms. The Iranians have internet too. And they can see all of this. They have now issued a fresh set of new demands: end sanctions, leave the region, pay reparations, release frozen assets and more — in addition to make the Strait of Hormuz a permanent Iranian toll road. More or less total capitulation.

One could imagine a scenario in which there was a tacit meeting of the minds between Trump and the Iranian government. Yes, Trump wants out. But as much as Iran has gained at the United States’s expense over the course of the war, it has also sustained a vast scale of damage to its civilian industrial base. Last winter’s protests were spurred by the already bad economy. So economic revival of some sort is critical to the regime’s medium and longterm survival. So Iran still has strong reasons to want to bring the conflict to an end. And yet they’re not. Trump’s desperation is so great that they are not taking that path. They’re upping the ante again and again. They think they have Trump over a barrel and they’re right. They want to hurt Trump as much as possible. And they don’t think they’ll pay much price for driving a hard and humiliating bargain.

Meanwhile, Israeli Prime Minister Benjamin Netanyahu is now openly rejecting the proposal put together by Trump’s “Board of Peace” which envisioned a staged process of disarmament by Hamas and Israeli withdrawals from Gaza. This is a more complicated story. In large part it is also a reflection of Trump’s ebbing power. But it also intersects with Israel’s election, which takes place on October 27.

Israeli politics have been in a state of crisis since 2022. For almost a year before the Hamas massacres in southern Israel, which began the war on and reoccupation of Gaza, weekly mass protests roiled the country. Since those attacks, Netanyahu has been consistently unpopular. But he had managed to claw back some of his support because of the Israeli successes against not only Iran but its proxies in the so-called “axis of resistance,” especially Hezbollah in southern Lebanon. But in recent months, Netanyahu has felt the inevitable downside of his alliance with Trump and, on a longer time scale, his alliance with the U.S. Republican Party — a point we’ll return to in another post.

Trump has made increasingly clear in public statements that he owns Netanyahu and, for that matter, Israel itself. He decides and Netanyahu complies, according to Trump. That is a particularly toxic claim in Israeli political culture, which prizes sovereignty and independence of action in the national security sphere almost above all else. That has taken all of Netanyahu’s other sources of domestic unpopularity and added two critical new ones. The first is that Netanyahu has become Trump’s poodle, according to Trump. The second is that Netanyahu placed all of Israel’s bets on Trump and the GOP. Now that looks like a questionable bet. Trump has grown tired of Israel’s demands. They’ve become inconvenient. And anti-Israel sentiment is growing within the GOP quite apart from Trump. The New York Times had this interesting article about how Israelis now fear that the loss of U.S. support isn’t a rough patch but permanent — something that many liberal Zionists including myself have been warning about for a generation. (Again, for another post.)

It’s in this context that Netanyahu has lots of reasons to resist this new deal. He might have done so anyway. He probably would have in substance. But Netanyahu is a past master at agreeing to and slow-rolling deals he wants to kill but can’t quite do so openly. Openly rejecting this deal is a choice and one driven by very specific domestic electoral weaknesses.

Netanyahu needs to show that he doesn’t answer to Trump. He needs to buttress and intensify support within the right-wing camp in Israel to have any hope of remaining in power after the next election. (The intensification of settler violence in the West Bank can also only be understood in electoral terms.) Picking a fight with Trump is critical to both aims. But if Trump didn’t look so weak at home he wouldn’t be doing it. As with Iran, Israel’s refusal to bend to Trump’s will goes back to his own declining popularity and power at home.

Zac Hall at 9to5Mac has a good rundown of new features and changes in beta 5. Some app icons got tweaks (the Siri app in particular looks much cooler now), and a bunch of the existing American and British Siri speaking voices now have the Pace and Expressivity adjustment sliders.

Also interesting: the OS 27 releases were stuck at beta 4 for 22 days. That’s a week longer than usual. Will Hains (my Kotoba friend) maintains a wonderful single-page website tracking iOS version release date history. For these summer “next big version” comparisons, it’s best to filter by “*.0” releases. Do that at Hains’s website and you can see a fairly clear pattern: betas 1 through 4 typically last about two weeks each; then starting with beta 5, Apple switches to a roughly weekly schedule until the end of the beta cycle. I wouldn’t read anything into that other than to expect beta 6 next week and beta 7 the week after that.

This afternoon, Emine Yücel, Josh Kovensky and John Light will join me on our YouTube channel to discuss their investigation from last week showing that the Trump administration has on multiple occasions withheld funds from blue states just because they voted blue — you know, the kind of story that would have been leading every news program for a month in the Before Times. Anyway, join us at 1 p.m. ET.

PSA: We’re going to be very active over on YouTube going forward. If you like hearing our voices and seeing our faces, please subscribe so you don’t miss anything!

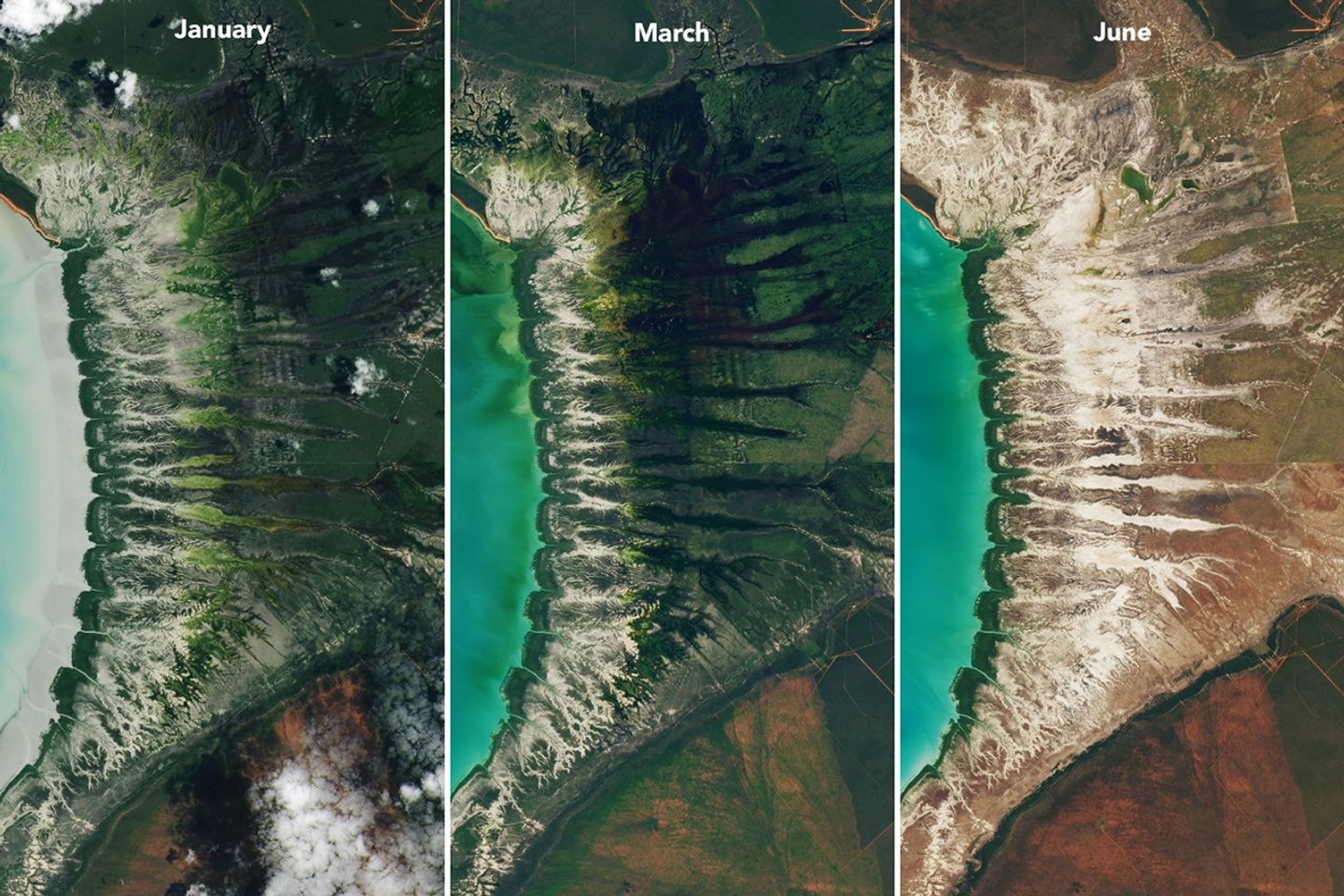

Water covers intertidal mudflats around Roebuck Bay in Western Australia, as seen in this image captured by the OLI (Operational Land Imager) on Landsat 8 on March 18, 2026.

NASA Earth Observatory / Lauren Dauphin

Editor’s Note: Today’s story is the answer to the August Puzzler.

Tides are among the clearest signs of the Moon’s pull on Earth. Just 239,000 miles (385,000 kilometers) away, the Moon’s gravity pulls on Earth’s oceans and solid crust, subtly distorting them into a more oblong shape with bulges roughly extending toward and away from the Moon.

High tides happen throughout Earth’s oceans, but in some places they leave an unusually strong fingerprint on the landscape. Among those places is Roebuck Bay, a crescent-shaped feature in the Kimberley region of Western Australia.

Roebuck Bay’s tidal range can reach a remarkable 9 meters (30 feet). Rising and falling tides repeatedly inundate and expose expansive mudflats, flood broad mangrove forests and salt marshes, and feed branching networks of tidal drainage channels. Many parts of Australia have tidal ranges of 2 meters or less. But the large range at Roebuck Bay is mostly a consequence of northwestern Australia’s unusually wide, shallow continental shelf, which helps amplify tides as they approach the coast.

The image at the top of the page shows the bay on March 18, 2026, when water levels were high. Green mangrove forests grow thickly along the shoreline and line the mouths of a network of evenly spaced, linear tidal creeks. These mangrove forests are dynamic. Analysis of decades of Landsat observations shows them expanding westward by nearly 2 meters per year as sediment from the waterways to the east accumulates in the sheltered bay.

Farther inland, branching networks of tidal drainage channels connect with the tidal creeks, giving the bay its feathered appearance. These channels, partially obscured by thick vegetation in March, were more visible earlier and later in the year, when vegetation was thinner.

Around Roebuck Bay, inland vegetation greens after monsoon rains, peaking in March, and turns brown and dry by June. The Landsat 8 and 9 satellites captured these images throughout 2026.

NASA Earth Observatory / Lauren Dauphin

Monsoonal rains, typically falling between December and March, transform the landscape around the bay into lush grasslands and seasonal wetlands. As the rains fade in May and June and the dry season takes hold, these ephemeral grasses and sedge ecosystems die back, turning the landscape shades of gold and brown. The consistent spacing of the tidal creeks is likely not a tidal effect; it appears to be influenced by the regular spacing of linear dunes in the broader region, as seen in the plains to the east.

The bay’s dramatic tidal and seasonal changes are striking from above, and they also support a bounty of life on the ground. The mangroves serve as nurseries for crustaceans and fish, and the mudflats teem with dozens of types of invertebrates, including snails, worms, crabs, clams, and cockles. Shells and snails can reach an abundance of 2,500 per square meter, according to the Australian government.

This bounty of marine life is a major draw for birds. The bay, one of the most important sites for migratory birds in Australia and a key stop on the East Asian-Australasian Flyway, regularly hosts hundreds of thousands of birds, including plovers, godwits, and knots.

NASA Earth Observatory images by Lauren Dauphin, using Landsat data from the U.S. Geological Survey.Story by Adam Voiland.

Downloads

January 29, 2026

JPEG (3.65 MB)

March 18, 2026

JPEG (3.41 MB)

June 20, 2026

JPEG (3.61 MB)

References & Resources

Birdlife International (2026) Roebuck Bay. Accessed August 10, 2026.

Brockmann Consult (2025) Roebuck Bay. Accessed August 10, 2026.

Kepler Communications plans to deploy next-generation optical relay satellites on Rocket Lab’s upcoming Neutron rocket in one of several launches the Canadian operator has slated for 2028.

HELSINKI — China appears to have lost an unknown payload after a Long March 7A rocket exploded less than 90 seconds into flight, according to amateur footage. The Long March […]

A decade ago, a United States carrier strike group departing San Diego could cross the Pacific with only intermittent detection. China might catch a glimpse — a satellite pass here, […]

The majority owner of Rocket Factory Augsburg is still confident the company will conduct its first orbital launch attempt this year despite a setback in testing.

WARSAW, Poland — The Lithuanian space laser communications company Astrolight has signed a memorandum of understanding with ATMOS Space Cargo, to demonstrate in-flight optical communications link between a reentry spacecraft […]

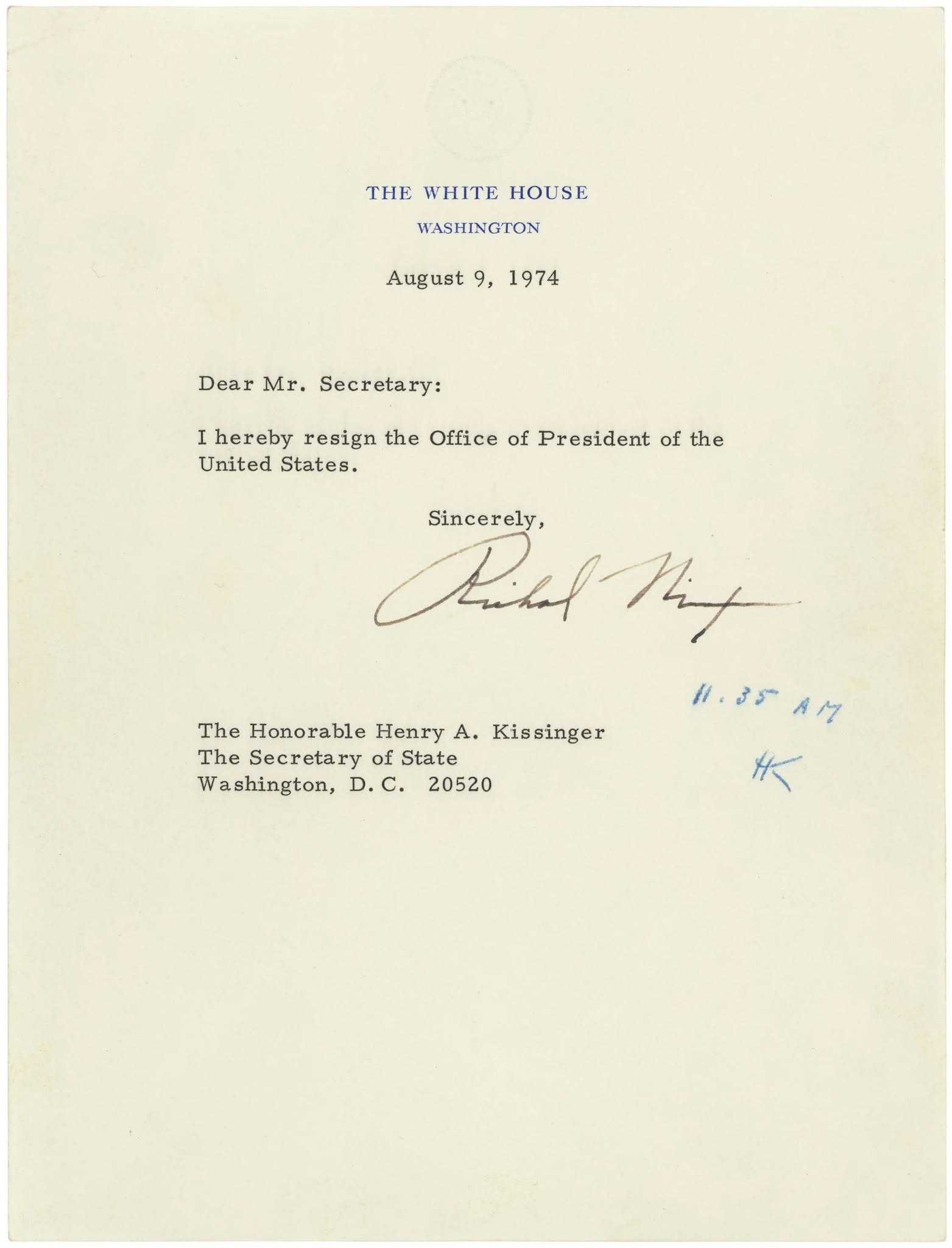

On August 9, 1974, Richard M. Nixon became the first president in U.S. history to resign.

The road to that resignation began in 1971, when Daniel Ellsberg, who was at the time an employee of the RAND Corporation and thus had access to a top-secret Pentagon study of the way U.S. leaders had made decisions about the Vietnam War, leaked that study to major U.S. newspapers, including the New York Times and the Washington Post.

The Pentagon Papers showed that every president from Harry S. Truman to Lyndon B. Johnson had lied to the public about events in Vietnam, and Nixon worried that “enemies” would follow the Pentagon Papers with a leak of information about his own decision-making to destroy his administration and hand the 1972 election to a Democrat.

The FBI seemed to Nixon reluctant to believe he was being stalked by enemies. So the president organized his own Special Investigations Unit out of the White House to stop leaks. And who stops leaks? Plumbers.

The plumbers burglarized the office of Ellsberg’s psychiatrist in California, hoping to find something to discredit him, then moved on to bigger targets. Together with the Committee to Re-elect the President (fittingly dubbed CREEP as its activities became known), they planted fake letters in newspapers declaring support for Nixon and hatred for his opponents, spied on Democrats, and hired vendors for Democratic rallies and then scarpered on the bills. Finally, they set out to wiretap the Washington, D.C., headquarters of the Democratic National Committee, in the fashionable Watergate office complex.

Early in the morning of June 17, 1972, Watergate security guard Frank Wills noticed that a door lock had been taped open. He ripped off the tape and closed the door, but on his next round, he found the door taped open again. Wills called the police, who arrested five men ransacking the DNC’s files.

The White House immediately denounced what it called a “third-rate burglary attempt,” and the Watergate break-in gained no traction before the 1972 election, which Nixon and Vice-President Spiro Agnew won with an astonishing 60.7% of the popular vote.

But Bob Woodward and Carl Bernstein, two young Washington Post reporters, followed the sloppy money trail back to the White House, and by March 1973 the scheme was unraveling. One of the burglars, James W. McCord Jr., wrote a letter to Judge John Sirica before his sentencing claiming he had lied at his trial to protect government officials. Sirica made the letter public, and White House counsel John Dean immediately began cooperating with prosecutors.

In April, three of Nixon’s top advisors resigned, and in May the president was forced to appoint former solicitor general of the United States Archibald Cox as a special prosecutor to investigate the affair. That same month, the Select Committee on Presidential Campaign Activities, informally known as the Senate Watergate Committee, began nationally televised hearings. The committee’s chair was Sam Ervin (D-NC), a conservative Democrat who would not run for reelection in 1974 and thus was expected to be able to do the job without political grandstanding.

The hearings turned up the explosive testimony of John Dean, who said he had talked to Nixon about covering up the burglary more than 30 times, but there the investigation sat during the hot summer of 1973 as the committee churned through witnesses. And then, on July 13, 1973, deputy assistant to the president Alexander Butterfield revealed the bombshell news that conversations and phone calls in the Oval Office had been taped since 1971.

Nixon refused to provide copies of the tapes either to Cox or to the Senate committee. When Cox subpoenaed a number of the tapes, Nixon ordered Attorney General Elliot Richardson to fire him. In the October 20, 1973, “Saturday Night Massacre,” Richardson and his deputy, William Ruckelshaus, refused to execute Nixon’s order and resigned in protest; it was only the third man at the Justice Department—Solicitor General Robert Bork—who was willing to carry out the order firing Cox.

Popular outrage at the resignations and firing forced Nixon to ask Bork—now acting attorney general—to appoint a new special prosecutor, Leon Jaworski, a Democrat who had voted for Nixon, on November 1. On November 17, Nixon assured the American people that “I am not a crook.”